In this exclusive, Navindu Katugampola, head of green and sustainability bond origination at Morgan Stanley, based in London opens up to PFR’s Managing Editor Nischinta Amarnath about the rationale behind the $500 million bond sale, the burgeoning market for green bond issuances and the flow of private capital towards green bond issuers in the U.S.

PFR: Tell me about the green bond origination team at Morgan Stanley and more about your role there.

KATUGAMPOLA: The green and sustainability bond origination team is part of a broader commitment to sustainable investing at Morgan Stanley. We formalized this in 2013 with the creation of the Morgan Stanley Institute for Sustainable Investing, and the institute essentially has three main focus areas. The first is capacity building – developing programs and strategic partnerships that build capacity and best practices in the field of sustainable investing. The second aspect is thought leadership – generating insights that help mobilize capital to sustainability solutions. And the third aspect, which is where we come in, is sustainable investing – developing financial solutions that enable sustainable investing at scale. That is the goal of green bonds. Over the last two to three years we’ve helped raise over $15.5 billion across 30 transactions for green and sustainability-focused projects. The main effort is coordinated globally from London. We have a large global sustainability finance team in New York where we also have people focused on the U.S. municipality space, a growth area for sustainable investing. We also have experts in Asia and LatAm who are focused on this. So, it’s a broad collective effort with individuals with regional expertise drawing upon the capabilities of the broader organization where relevant.

PFR: How do you see your current role evolving within the green bond origination team, going forward?

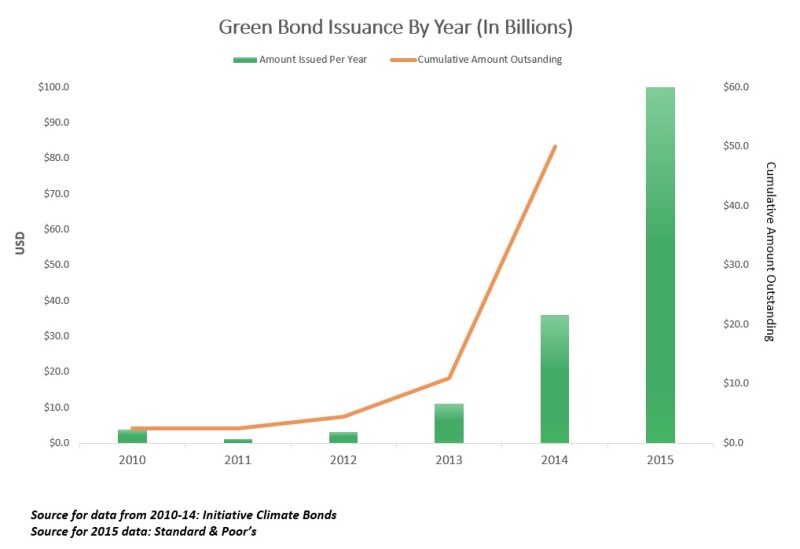

KATUGAMPOLA: This market has grown significantly over the last few years. We went from a market that was only really a few hundred million dollars at best, going back three or four years ago. Over the course of 2012 it grew to over $1 billion; in 2013 it was over $10 billion, and then last year, it grew to a size well in excess of $30 billion. This growth has been driven by a broader range of issuer types, issuer industries and issuer geographies within the green and sustainability bond space. In terms of how I see the role evolving, it will focus on delivering capital raising and sustainable investment solutions that can further activate this growing universe of potential issuers.

PFR: What was the rationale behind the launch of the $500 million green bond from Morgan Stanley?

KATUGAMPOLA: Our work as an underwriter of green bonds has already helped direct billions of dollars towards environmentally and socially responsible projects. The rationale for issuing our own green bond was to bring what we’ve helped develop and learned from this market, and show how any issuer, regardless of industry, can make use of this financing tool to help support projects that can help generate positive environmental or social impact. So, the Morgan Stanley green bond was at the heart of our corporate ethos and our strategy around sustainability, and was underpinned by the expertise we developed over the last few years with the transactions we led.

Our selection of assets around renewable energy and energy efficiency focused on renewable energy, in particular wind and solar energy, and energy-efficiency projects, so that the projects we selected could meet the broadest appeal in terms of investor interest.

PFR: What are the key objectives in terms of your focus on the wind market in Texas?

KATUGAMPOLA: Texas is becoming a compelling site for wind farm development in particularly thanks to a $7 billion investment by the state into a 3,600-mile-long network of high-voltage transmission lines. What that does is link the Panhandle and West Texas areas to consumers in the Dallas, Austin and Houston areas.

PFR: In terms of proceeds of the $500 million green bond issuance being channeled to green project investments, how does that tie into generation projects such as wind farms?

KATUGAMPOLA: In terms of Morgan Stanley’s renewables portfolio, we identified a portfolio of projects – over the course of the last 12 months, as well as on a forward-looking basis – whose notional value comfortably exceeded the notional value of the bond. This gave us comfort that the funds we raised could indeed be allocated to projects.

PFR: How do green bonds differ from other Morgan Stanley bonds?

KATUGAMPOLA: The primary difference is how the proceeds from the green bond will be allocated. To be sure, it’s the same as other Morgan Stanley bonds in that it has the same level of creditworthiness as other Morgan Stanley bonds. What’s different is that by raising $500 million, we expect to allocate an equivalent amount in projects matching our green bond criteria and the proceeds of the offering will remain in a segregated account until such allocations are made.

PFR: What is the biggest challenge you faced in your career with Morgan Stanley?

KATUGAMPOLA: Markets evolve, and it’s important to be dynamic and proactive in how you respond to them. The growth of the green and sustainability market is a clear example of that, and there we saw both a challenge and an opportunity. When the green and sustainability market started taking off, we made a conscious decision at Morgan Stanley to proactively pursue the opportunity because of what it signified – an opportunity to direct capital toward positive social and environmental projects.

PFR: What about challenges in terms of competition?

KATUGAMPOLA: I don’t think competition is a bad thing at all. Ultimately, we have to remember what this product is helping to achieve, driving capital toward sustainable investing. That, in my mind, is only a positive thing. And I think the more people that are involved – and by that I mean the more issuers, underwriters and investors – the better. To be blunt, I would much rather we at Morgan Stanley had a smaller piece of a much larger market than a monopoly in a very small market, because ultimately what we are trying to do here is bigger than just league-table ambitions. It’s actually trying to transform the way people perceive finance as something that can result in positive social and environmental benefits.

PFR: Who are the key takers you see for green bonds today?

KATUGAMPOLA: What may surprise some is that green bonds are applicable to a very wide range of companies. Any issuer from any industry across any geography can take a look at how they conduct their business and ask themselves how they can do it in a more sustainable, more environmentally-friendly way – then try to see whether the green and sustainability bond market can help them draw capital to help achieve those sustainability goals. We’ve helped issuers across many industries, not just in the energy space but also we have worked with Unilever, the multi-national consumer goods company, and with BRF SA, the Brazilian food company.

PFR: What is your view on the flow of private capital towards green bonds in the U.S.?

KATUGAMPOLA: There is huge demand for this at the moment within the U.S. To give you some perspective on it, our Wealth Management division regularly conducts investor-pulse polls to get a sense of how our clients are thinking about the world and the key issues on their minds. It’s fair to say that a majority of people now realize that climate change is a real and present problem, with 71% of the people that we surveyed saying humans are having at least some impact on climate change. More interestingly, 30% of them said that climate change is impacting the value of their investments or portfolios as well. That’s quite a powerful statement. Individual investors are very focused on these issues and I think that is a trend that is going to be growing within the U.S. in particular. It is also representative of what we in the green bond origination team have seen with our own client base – corporates, municipalities, financial institutions.

PFR: Where do you see the green bond market heading (i) in the U.S. power sector, and (ii) globally? What other advantages do green bonds offer investors?

KATUGAMPOLA: I see the green bond market becoming much broader than just renewable energy and power. I think the real growth opportunity is with wider industries and wider geographies as evidenced by our own transaction. Again, Unilever is a fast-moving consumer-goods company that also issued a green bond. So I think the opportunity for growth is much broader than just the energy sector.

The main advantage for green bond investors is not tax benefits – because, liked fixed income more broadly, only some green bonds have tax benefits – but rather it is the opportunity to have transparency around how capital is being directed and what that capital is achieving. The whole idea around the green bond is to have transparency around the projects from day one by highlighting what projects are eligible for investment and on an ongoing basis by providing regular reporting. To be sure, investors in our green bond are not participating in risk sharing. Regardless of how these projects perform, it doesn’t affect the return that the investors get.

PFR: Are all the projects of the green bond origination team contracted? Or are there any merchant projects that are being considered as well?

KATUGAMPOLA: Our green bond origination team works primarily with issuers rather than the underlying projects. So, we don’t actually get involved with the specific end-projects. It’s up to the issuers of the green bonds who will be making those investments to approach us with respect to see how the green bonds can be applicable for them.

PFR: Issuers are vying to come to market ahead of an expected rise in the Federal Fund rate after September this year. What effects does this have on the green bonds market?

KATUGAMPOLA: The reality is that everyone realizes we will be going into a rising-rate environment. The only question is when, rather than if. In this regard, green bonds are like any other bonds and will be relevant even in that rising-rate environment because fixed-income investors have capital to put to work. So, I don’t think it makes any difference one way or the other.

PFR: What sorts of deals is your team looking to be a part of in the future?

KATUGAMPOLA: I think the way this market grows is laterally. So, we will be focusing on a broader range of issuers rather than more issuance from the same issuers. We’re very keen to talk to any potential new issuers of this product to see if this is something that could be relevant to them.

PFR: What are the key criteria you are looking for in terms of borrowers that approach the green bonds origination team?

KATUGAMPOLA: The main theme we are looking for is commitment and motivation. The green bond is a product in an area that you want to take seriously in order to do it the right way. If you’re happy to do that, it is a conversation we certainly want to have to see how we can help and whether the product will be relevant to your larger sustainability strategy.

PFR: What approaches do you follow to expand your clientele—in this case, your issuers?

KATUGAMPOLA: We are very much guided by the Green Bond Principles that lay out recommended guidelines on how to approach the green-bond market. That is our starting point, but beyond that we don’t have any prescriptive criteria. So, we are keen to have conversations with issuers interested in the product and see what it can deliver for them.

***